Taking The Right Amount of Risk: The Hidden Equation Behind Every Great Decision

Every moment of your life is a wager. You bet your time, your reputation, your money, your effort. You risk failure, embarrassment, or loss, all in the hope of gain.

Every moment of your life is a wager. You bet your time, your reputation, your money, your effort. You risk failure, embarrassment, or loss, all in the hope of gain. Most people don’t realize that what separates the fortunate from the forgotten isn’t luck or genius, it’s risk calibration.

The best lives are built not by avoiding risk, but by mastering it. There is a right amount of risk to take, measurable, teachable, and repeatable, and in the next twenty minutes, you’ll learn how to calculate it.

This short course teaches how to find your personal balance between courage and caution using the same principles that govern nature, evolution, and civilization itself. Along the way, you’ll pick up key terms from Natural Law, the universal grammar of cooperation and survival.

1. Life Is Risk: You Can’t Opt Out

Why this section exists: To reframe risk as natural, necessary, and moral, not something to be feared, but something to understand.

Every breath, every choice, every heartbeat is an act of risk management. Life is a constant trade between safety and opportunity. Risk isn’t your enemy, stagnation is. You can’t eliminate uncertainty, but you can measure and balance it.

We are constantly fighting entropy, the universal tendency of systems to decay, lose energy, and drift toward disorder. In physics, entropy measures the gradual breakdown of order into randomness; in life, it describes how our bodies age, our skills fade, and our societies weaken without continual renewal. Every act of effort, learning, and adaptation pushes back against this decay.

Stagnation is surrender to entropy: doing nothing guarantees that disorder and decline will win. Every choice we make either loses slowly to entropy or resists it by investing energy and intention into creating order, growth, and resilience. There is no safe option of doing nothing; safety is always temporary because entropy never stops working against us.

Definition (Operational): Risk is the measurable possibility that an action, decision, or event will produce a deviation between expected and actual outcomes, a potential loss or gain relative to your invested time, energy, or resources.

Relationship to investment: Risk and investment are inseparable. Every investment, whether of time, attention, energy, or material resources, is a choice to expose yourself to uncertainty in pursuit of greater return. Investing is how you commit to a path of growth; risk is the uncertainty that makes that investment meaningful. The more effectively you manage your risk, the more efficiently your investments compound over time, not just in wealth, but in experience, skill, and cooperation.

Natural Law concept: Demonstrated Interests, Every action you take reveals what you value most at that moment. Choosing safety over opportunity, or vice versa, demonstrates your real priorities.

The most successful organisms, and civilizations, are those that take bounded risks: risks large enough to grow, but small enough to survive the losses.

Rule #1: The only way to live without risk is to stop living.

2. The Math of Risk: Measuring the Unseen

Why this section exists: To give you a formula for understanding uncertainty, the same logic that underlies evolution, finance, and law.

Most people throughout history managed risk through instinct. Those whose instincts failed often didn’t survive long enough to pass on their habits. For millennia, the human species evolved its intuition for risk through trial and error, feedback, and experience. But in the modern world, we are insulated from most direct dangers. Fewer people experience physical, social, or financial consequences early enough to train their instincts. As a result, many grow up without an internal sense for how much risk is right.

That’s why it helps to have a formula. The goal isn’t to turn life into an equation, it’s to use the math to train your gut. You don’t need to calculate every small decision. But if you can run this formula on your bigger life choices, you can begin to see how natural risk-takers, entrepreneurs, explorers, leaders, think intuitively. Over time, this trains your instincts to make smaller, faster, lawful decisions about risk in daily life.

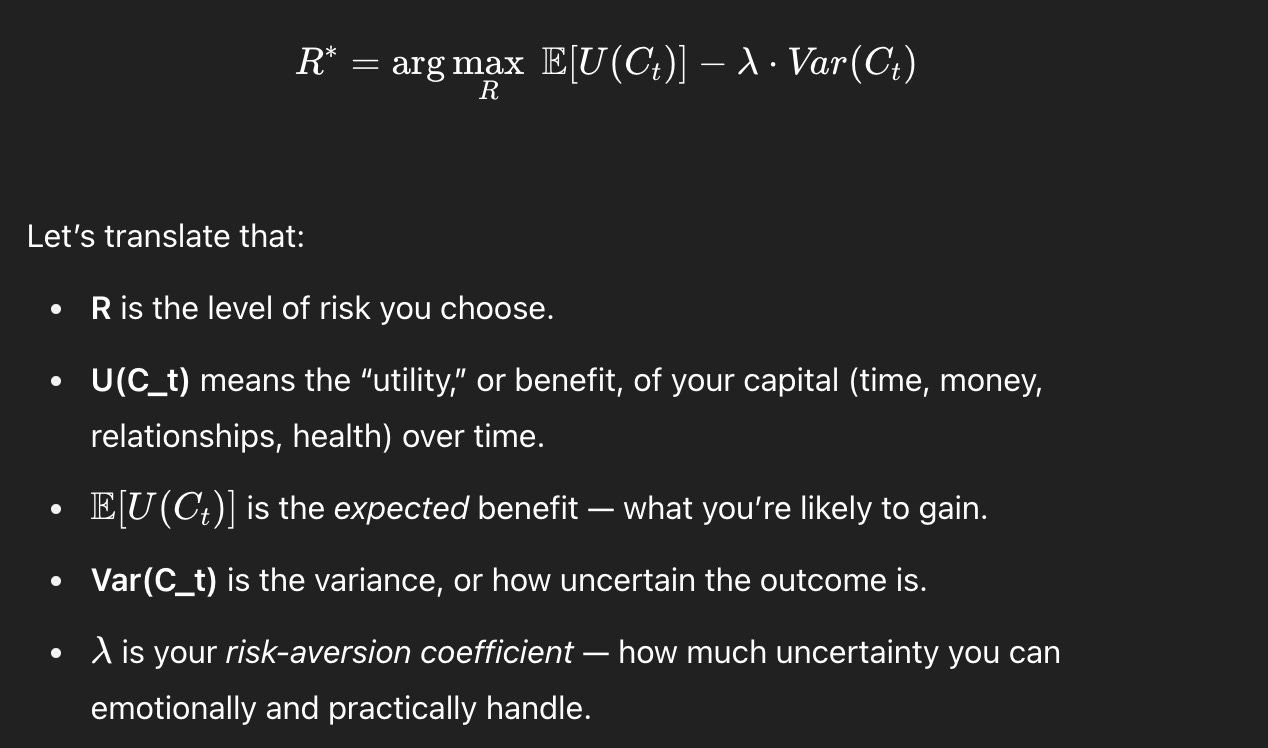

Here’s the simplified formula for optimal risk:

You are always balancing expected gain against uncertainty.

The sweet spot, (R*), is where one more unit of risk no longer increases your long-term return.

In Natural Law terms: You’re computing your reciprocity with reality, the point where your efforts and nature’s feedback remain in balance.

Rule #2: Take as much risk as you can afford to insure, as much as you can recover from, and no more.

Where this math comes from: This equation is drawn from fields like statistics, probability theory, decision theory, and economics. It blends concepts of expected utility and variance to model how rational agents make trade‑offs between reward and uncertainty. In simple terms, it’s the same logic used in evolutionary biology, financial portfolio management, and any system that optimizes growth under uncertainty.

Disclaimer: If you notice I’ve made a mistake in the math, please explain to me as clearly as you can what I need to do to fix it. You can either write in the comments below or message me directly, I appreciate the help.

3. The Principle of Bounded Risk

Why this section exists: To explain why unlimited risk destroys both individuals and civilizations, and why bounded risk creates sustainable growth.

Nature rewards those who experiment, but punishes those who overextend. Every species, every market, every empire operates under the same law: adapt, but don’t collapse.

The human brain evolved to manage bounded risk, to test, learn, and adapt in cycles. You learn to walk by falling safely. You learn to love by risking trust. You learn to lead by risking failure. The key is recoverability.

Any risk you can’t measure is, by definition, unbounded. The level of risk appropriate for one person may not be the same for another because each of us operates under unique capacities, experiences, and tolerances. This means the calculation of risk must always be personal. It’s difficult for anyone else to determine your optimal level of risk because they’ll inevitably apply their own biases and preferences. Learning to measure and manage your own risk is therefore an essential skill, one that builds both autonomy and judgment.

Vocabulary highlight: Insurability, the ability to bear the cost of a mistake without transferring it unfairly to others. Don’t risk what you can’t afford to lose.

A lawful person, under Natural Law, takes risks they can insure and does not externalize losses onto others. This is the moral dimension of risk: reciprocal responsibility.

Rule #3: The moral limit of risk is the point where your losses would make others pay.

4. De-Risking: How to Lower Risk So You Can Take More of It

Why this section exists: To teach that risk-taking is not recklessness; it’s engineering, and preparation expands freedom.

You can’t eliminate risk, but you can make it smaller relative to your capacity. That’s what insurance, in every form, does. Insurance isn’t just compensation if things go wrong; it’s also every measure you take to prevent things from going wrong in the first place. Real insurance is preparation and resilience, designing your choices so that even if your risk doesn’t pay off the way you intended, it still produces some form of profit or learning. It’s about structuring life so that every outcome moves you forward, even if not in the way you planned.

Four Forms of Insurance:

Material Insurance – savings, tools, and skills that absorb shocks.

Social Insurance – trust, reputation, friendships that share burdens.

Moral Insurance – truthfulness, reliability, and reciprocity that make others willing to insure you.

Institutional Insurance – legal and cooperative systems that enforce fairness and restitution.

De-risking isn’t cowardice, it’s leverage. A person who prepares can take on risks that would destroy someone else and get benefits that seem out of reach to others.

Rule #4: Preparation gives us the power to survive failure.

Vocabulary highlight: Reciprocity, the universal moral law of equal return for equal cost. In risk terms: don’t take what you can’t give back.

5. Case Studies: The Three Levels of Risk

Why this section exists: To make the abstract concrete, to show what “too little,” “too much,” and “just right” risk look like in real life, history, and civilization.

Too Little Risk

Personal Example: A student chooses an easy path, a safe major, a stable job, and avoids failure. Ten years later, they’re secure but stagnant. Their life’s variance is zero, but so is its growth.

Historical Example: The Ming Dynasty sealed its borders, avoiding exploration after Zheng He’s voyages. Risk-avoidance preserved stability, and ceded the future to Europe.

Civilizational Example: Byzantium perfected defense but lost innovation. Safety became fragility.

Lesson: Safety without adaptation leads to decay. Nature punishes stasis.

Too Much Risk

Personal Example: A young investor bets everything on crypto at the peak. No margin, no insurance, no plan. One market cycle later, ruin.

Historical Example: Napoleon, unmatched genius, but overextended ambition. His empire collapsed because he violated bounded risk.

Civilizational Example: Rome’s expansion beyond governable limits created internal entropy and moral collapse.

Lesson: Unbounded risk converts brilliance into catastrophe.

Just Right

Personal Example: A small business owner reinvests 20% of profit each year, keeps reserves, and experiments carefully. Growth compounds.

Historical Example: George Washington, bold in action, conservative in logistics. He took risks he could survive, and so founded a nation.

Civilizational Example: Early modern Europe, competition among bounded states fostered innovation without single-point collapse.

Lesson: The right risk builds continuity, the bridge between today’s effort and tomorrow’s possibility.

Rule #5: Adaptation = experiment within your margin of safety.

Example: Theodore Roosevelt and the Strenuous Life

Theodore Roosevelt entered the world in frailty. Born small and sickly, he gasped for air with every breath, wracked by asthma and weakness. Doctors warned his family that the boy should avoid strain and exertion. But young Roosevelt, fiery even then, looked upon his reflection and made a vow: if nature had denied him strength, he would build it himself.

He built a gym in his bedroom and forced his body through relentless exercise. Every pull of the bar and every drop of sweat was an act of rebellion against fragility. He learned to box, to ride, to hike mountains and break horses. Each of these was a risk, but it was bounded, calculated. He strengthened the structure before testing it, preparing his body and mind so thoroughly that adventure became not recklessness but method.

That preparation forged a man who led from the front. When war came, he rode with the Rough Riders up San Juan Hill, his courage magnetic, his preparation contagious. On the eve of battle, Roosevelt assessed the terrain, the morale of his men, and the exposed approach to the heights. He divided his forces, coordinating flanking fire to reduce exposure, and insisted on reconnaissance before advancing. He rode with his men, deliberately on horseback to serve as a visible anchor of calm amid chaos, a calculated move to steady their nerves though it made him a target. When his unit came under withering Spanish fire, he ordered a measured advance, halting twice to reform and redistribute ammunition, preventing panic and conserving strength for the final surge. Each decision balanced aggression and preservation; each action turned danger into momentum. His men trusted him because his risks were shared and disciplined. He taught them that boldness, without calculation, was suicide, but boldness with preparation was triumph.

Even later, when his presidency could have ended in comfort, Roosevelt again reached beyond safety. He ventured into the unmapped Amazon on the River of Doubt, a journey that nearly killed him. Before departure, he prepared obsessively: studying maps, calculating supply weights, and choosing seasoned guides and scientists for the team. He secured diplomatic clearance through Brazil, arranged native support, and personally funded redundancies in food and medical stores. His insistence on thorough logistics was a de-risking strategy, ensuring that failure, if it came, would be survivable.

Once in the jungle, Roosevelt applied the same bounded risk logic he’d practiced all his life. When the expedition confronted impassable rapids, he ordered portages rather than gambling lives on reckless runs. When disease and exhaustion struck, he rationed food to preserve endurance and halted progress until discipline was restored. Even as fever wracked his own body, he delegated command to protect the mission’s chain of responsibility. Each decision measured courage against consequence, adventure against continuity.

Every decision, every ration, every plan reflected mastery of risk: enough daring to discover, enough discipline to survive. His courage inspired not only his companions but a generation. He transformed the American image from cautious prosperity to vigorous striving, from safety to effort.

Through his example, Roosevelt showed that courage and preparation together could lift a man, and a nation, beyond its limitations. He taught that risk, when managed with foresight and honor, is not just survival but creation. His Strenuous Life became the American life: proof that when we prepare deeply and act boldly, our risks do not destroy us; they remake us into something greater.

6. The Moral Logic of Risk

Why this section exists: To tie personal courage to moral law, showing that taking the right amount of risk isn’t just smart, it’s ethical.

Risk-taking is a duty to life. It is how the universe evolves. Every act of responsible courage increases knowledge, wealth, and cooperation. This is true because the process of evolution, biological, intellectual, and social, depends on variation, experimentation, and adaptation. Each act of risk introduces a new possibility into the system, creating information about what works and what fails. When we take responsible risks, we feed the universe with data that helps it organize at higher levels of complexity. On the personal scale, risk-taking refines judgment and builds competence. On the civilizational scale, it drives discovery, innovation, and cooperation. Without risk, no learning occurs; without learning, the universe cannot evolve toward greater order and potential.

But all lawful risk-taking must meet three tests:

Reciprocity: Others aren’t forced to bear your costs.

Testifiability: You can explain your decision clearly and truthfully.

Insurability: You can recover without harm to the group.

When people or institutions take risks that fail these tests, they act parasitically, socializing the losses, privatizing the gains. Civilization decays when such behavior goes unpunished.

Vocabulary highlight: Decidability, the ability to reach a true and testable conclusion without discretion or bias. In risk, it means knowing when an outcome can be judged objectively.

Rule #6: Lawful risk is reciprocal, testifiable, and insurable.

7. How to Live Lawfully in a Risky World

Why this section exists: To synthesize principles into daily practice, to help the reader turn knowledge into action.

The world doesn’t reward those who take the safe path; and it punishes the foolhardy. Only those rightly calibrated will see great success. Risk is the engine of progress, and fear is its brake. You need both. Your life’s goal is not to eliminate risk, but to choose it wisely. This is true because life is an ongoing process of experimentation, a continuous search for the right action in ever‑changing conditions. We will not always get it right; miscalculations are inevitable. Yet each failure is information, each mistake a new data point that refines your judgment. The goal is not to repeat the same errors, but to make new, wiser, and more prosperous ones. Progress depends on this endless cycle of risk, reflection, and recalibration, a process that never ends so long as life itself continues.

Five-Step Daily Risk Practice

Identify your demonstrated interests — what you truly value.

Estimate the expected gain and possible loss.

Prepare your insurances — material, social, moral, institutional.

Take the bounded risk — act within recoverable limits.

Review outcomes — adjust your future risk coefficient.

Rule #7: Risk intelligently, fail gracefully, adapt continuously.

The greatest civilizations, the best companies, and the happiest individuals all follow the same law: They measure, insure, and renew their risks.

You can too.

Conclusion: The Law of the Calculated Leap

Every step forward in history, from the first fire to the first flight, began as a calculated leap. The same logic applies to your life.

Nature rewards those who balance risk and restraint, courage and caution, ambition and humility. Take risks you can insure, learn from the feedback, and let the universe compute your success.

That’s the law of life, and the right amount of risk is its measure.

Now it’s your turn. Start taking the kind of risks that move your life forward, the risks you can prepare for, measure, and recover from. Every challenge you accept is a step toward greater strength and understanding. Don’t hide from uncertainty; train with it. De-risk your ambitions through preparation, practice, and honesty, then act decisively. The universe rewards motion, not hesitation.

If you’re unsure how to calculate what the right amount of risk is for you, don’t go it alone. Reach out for help, talk to mentors, friends, or professionals who can help you see what you might miss. Learning to calibrate your risk isn’t a one-time event; it’s a lifelong discipline. Begin now, and keep refining your judgment. Your future, and the civilization you contribute to, depend on your willingness to act with courage and care.

Glossary of Key Terms

Adaptive: The ability to adjust actions and strategies in response to feedback and changing circumstances.

Bounded Risk: Taking risks that are limited and recoverable; the amount of uncertainty one can bear without catastrophic loss.

Capital: Any stored value — time, energy, skill, knowledge, money, that can be invested to create future gains.

Decidability: The capacity to reach a clear, testable conclusion based on evidence and reason rather than opinion.

Demonstrated Interests: Actions that reveal what someone truly values, regardless of what they claim to value.

Entropy: The natural tendency of systems toward disorder and decay; in life, it represents the forces that cause decline unless resisted by work and learning.

Expected Utility (E[U(Cₜ)]): A mathematical term representing the average benefit expected from a decision over time.

Insurability: The ability to bear the consequences of a failed risk without transferring them unfairly to others.

Investment: The deliberate allocation of resources (time, energy, or material) in pursuit of a greater or future return.

Reciprocity: The moral law of equal return for equal cost; ensuring that benefits and burdens are shared fairly.

Risk: The measurable possibility that an action or decision will deviate from the expected result, producing loss or gain.

Risk-Aversion Coefficient (λ): A measure of how much uncertainty an individual can tolerate emotionally and practically.

Variance (Var(Cₜ)): The degree of unpredictability or spread in possible outcomes; higher variance equals higher risk.

The Strenuous Life: Theodore Roosevelt’s philosophy of embracing disciplined effort, bounded risk, and courageous action to achieve personal and social excellence.